An insurance denial feels personal, but it is usually built around one of a few categories: fault, coverage, medical causation, documentation, policy limits, or claim procedure. The right response depends on which reason the company gives and whether that reason is supported by the evidence.

This guide explains why insurers refuse payment, what to do next, and how Delventhal Law Office reviews denied or stalled Indiana car accident claims.

Key takeaways

- Get the denial or low-payment reason in writing.

- Separate liability disputes from coverage disputes and medical-causation disputes.

- Do not miss Indiana deadlines while arguing with an adjuster.

- Insurance complaints may address company conduct, but they do not replace an injury claim.

- A denial can often be challenged with better evidence, legal pressure, or litigation when appropriate.

Why insurance companies refuse to pay after an Indiana car accident

Common reasons include:

- Fault dispute: the insurer says its driver did not cause the crash or says you were partly or mostly at fault.

- Coverage problem: the policy was cancelled, excluded, too small, or does not apply to the vehicle or driver.

- Medical causation dispute: the insurer argues your symptoms came from a prior condition, later event, treatment gap, or low vehicle damage.

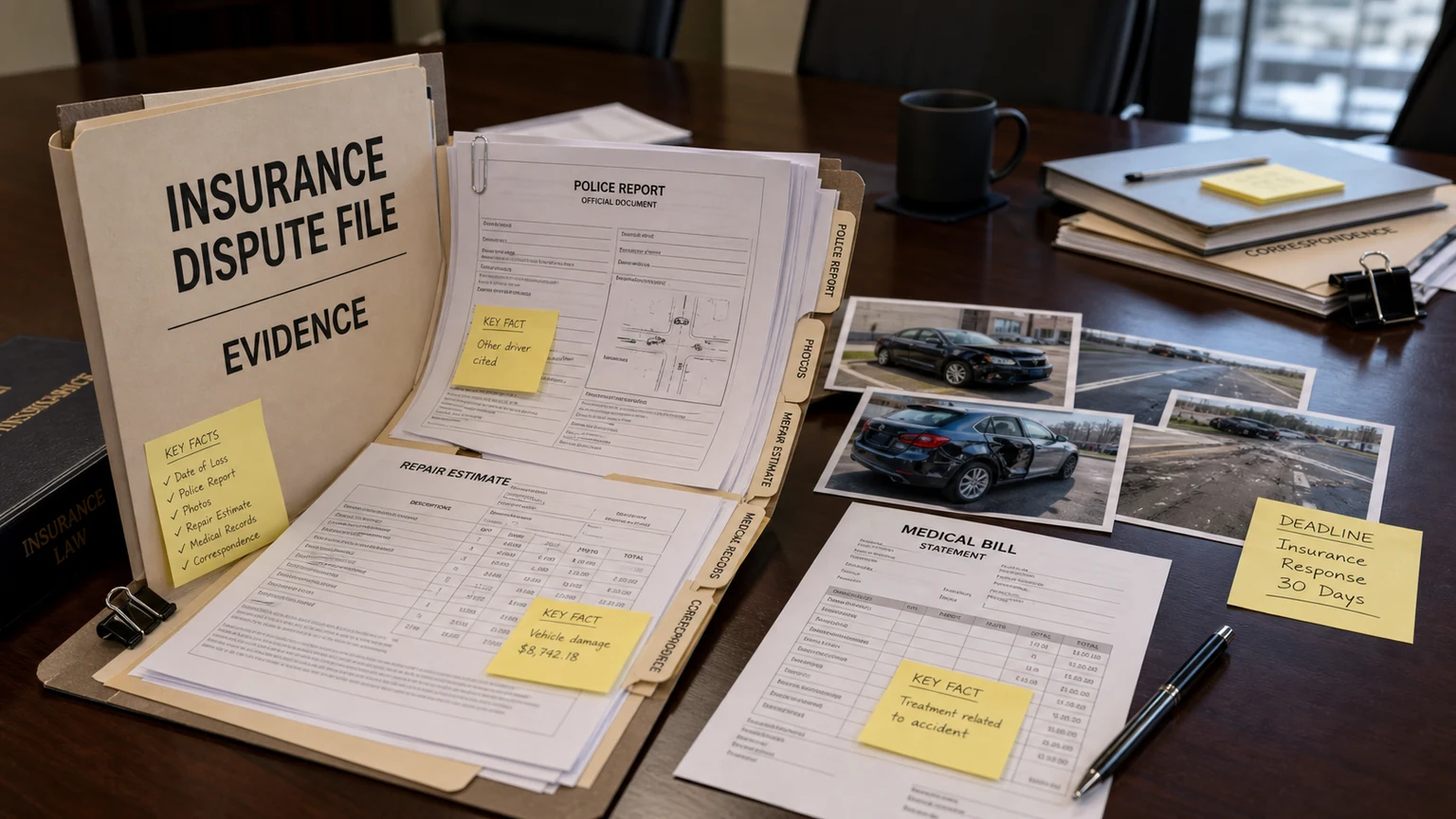

- Documentation dispute: bills, records, wage proof, photos, repair estimates, or lien information are missing.

- Policy-limit issue: the damages may exceed available liability coverage, especially with minimum insurance.

- Release or procedural issue: the insurer claims a form, proof, statement, or deadline has not been satisfied.

Indiana’s unfair claim settlement practices statute, Indiana Code § 27-4-1-4.5[1], addresses insurer conduct such as failing to acknowledge communications reasonably promptly, refusing to pay without reasonable investigation, and failing to provide a reasonable explanation for denial or compromise offers. Whether that statute changes your practical options depends on the facts and the type of claim. You can use our Indiana car accident settlement calculator to organize the factors that may affect a claim’s value; it is an educational tool, not a promise of any result.

First steps if the insurer says no

- Ask for the reason in writing. A vague phone explanation is easy to change later.

- Request the claim number, adjuster name, and policy information. You need to know which coverage is being discussed.

- Do not sign a release. A release usually ends the injury claim even if you later discover more bills or wage loss.

- Preserve evidence. Keep the vehicle photos, dashcam footage, repair documents, medical records, bottles, braces, and damaged personal items.

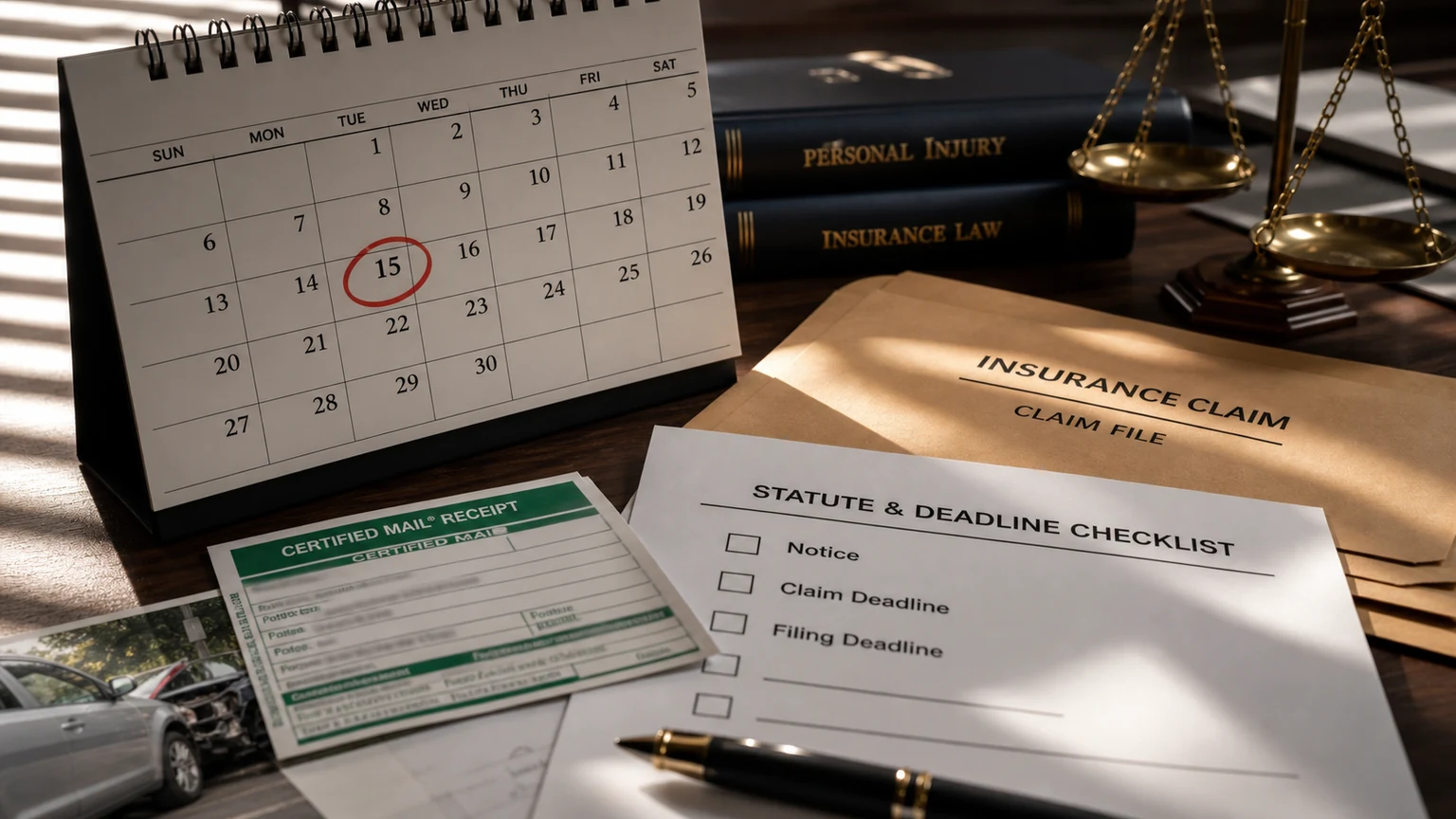

- Check deadlines. Indiana personal injury claims generally have a two-year lawsuit deadline under Indiana Code § 34-11-2-4[2], but shorter notice rules can apply to government-related claims.

- Organize the missing proof. Denials based on “insufficient documentation” can sometimes be challenged with a better packet.

If the adjuster wants a recorded statement or broad medical release, review Delventhal’s guide on recorded statements and medical releases after an Indiana accident before responding.

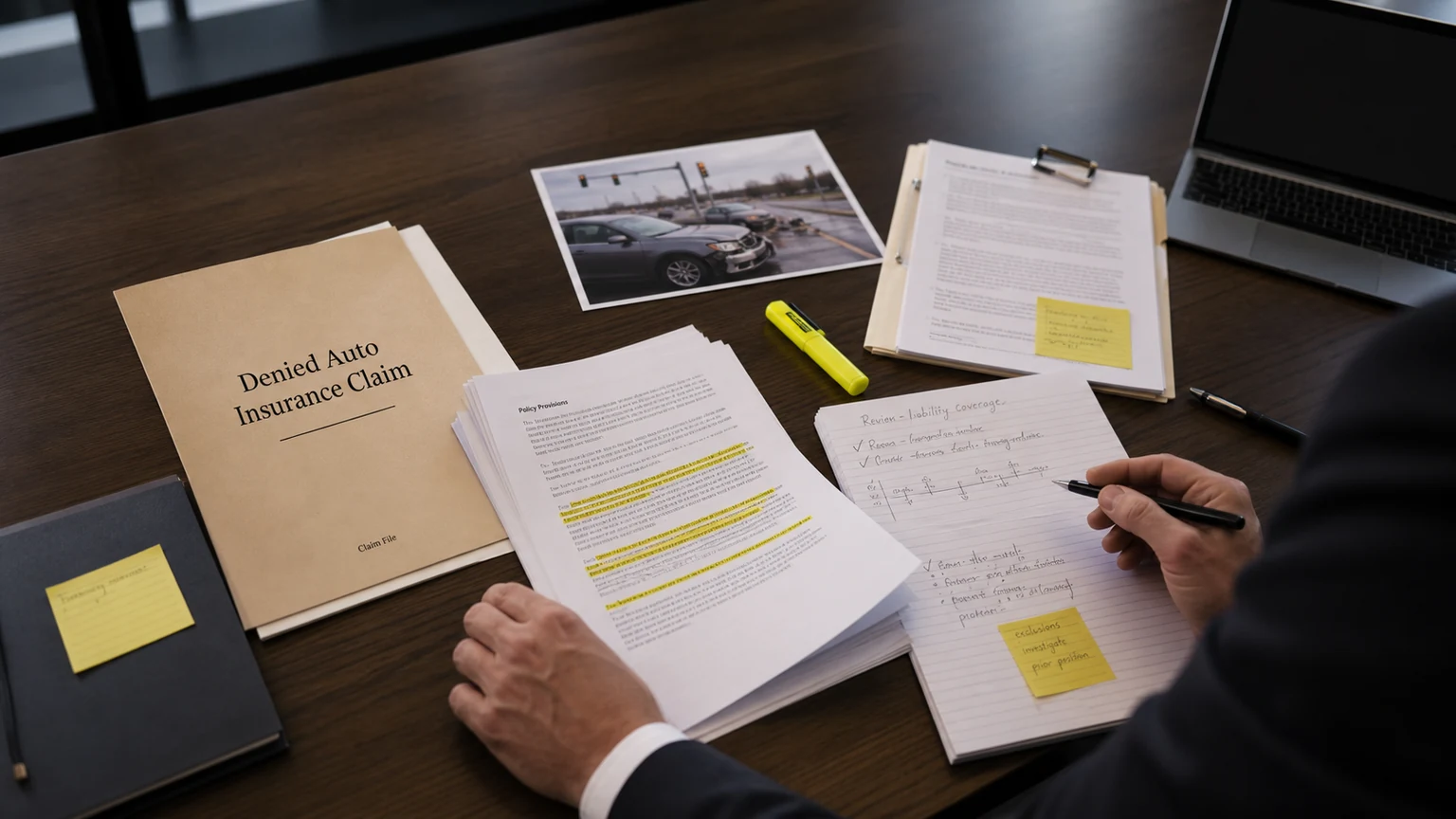

How to think about coverage, fault, and medical disputes

Coverage disputes

A coverage denial may involve cancellation, excluded drivers, business use, late notice, permission to drive, rideshare activity, or policy limits. If the at-fault driver has minimum limits, another Delventhal guide explains what happens when the other driver only has Indiana minimum insurance. Your own UM/UIM or MedPay coverage may also matter.

Fault disputes

Fault denials should be tested against the evidence. The police report matters, but it is not always the whole case. Photos, vehicle positions, skid marks, video, witness statements, phone records, roadway design, construction-zone facts, and crash reconstruction may matter. Indiana comparative fault can reduce or bar recovery in many claims under Indiana Code chapter 34-51-2[3]. Delventhal’s related guide covers police-report fault disputes.

Medical causation disputes

Insurers often argue that pain is from degeneration, a prior injury, delayed treatment, or minor vehicle damage. The response may require complete records, prior medical context, consistent symptom history, treating-provider opinions, imaging, therapy notes, and a clear timeline. Delventhal’s article on treatment gaps explains one common insurer argument.

Insurance complaint, lawsuit, or both?

The Indiana Department of Insurance[4] accepts consumer complaints about insurance issues. A complaint may help address claim-handling conduct, communication, or regulatory concerns. But it is not the same as filing a personal injury lawsuit, proving damages, or stopping the statute of limitations.

If the issue is that the other driver’s insurer simply refuses to accept liability or offer fair value, the practical remedy may be legal negotiation, a demand package, mediation, or lawsuit. Lawsuit strategy depends on liability evidence, damages, coverage, deadlines, venue, and whether litigation costs make sense for the claim.

When a lawyer should review a denied or stalled claim

Legal review matters when the insurer blames you, denies coverage, claims your injuries are unrelated, refuses to disclose limits, offers far less than the medical and wage evidence suggests, asks for broad authorizations, or the deadline is approaching. A denial does not mean the case is strong, but it does mean the next move should be deliberate.

Delventhal Law Office reviews car accident claims for people in Fort Wayne, Allen County, DeKalb County, Auburn, and northeast Indiana. The first step is usually to identify the denial reason, collect the missing evidence, and decide whether the claim can be fixed through documentation or needs legal pressure. Call 260-484-6655 or use the free case evaluation form.

FAQ: insurance company will not pay after an Indiana car accident

What should I do if the insurance company will not pay after an Indiana crash?

Ask for the reason in writing, gather missing proof, avoid signing a release, preserve deadlines, and consider legal review if liability, damages, or coverage is disputed.

Can an insurer deny a claim because it says I was partly at fault?

Yes, insurers often use comparative fault arguments to reduce or deny payment. The argument should be tested against the crash evidence, not accepted at face value.

Can I complain to the Indiana Department of Insurance?

You may be able to file a consumer complaint about insurer conduct, but a complaint is not the same as pursuing your injury claim or preserving lawsuit deadlines.

Does a denial mean my case is over?

No. A denial may reflect missing documentation, a coverage dispute, a fault dispute, or negotiation posture. The next step depends on the reason given and the evidence available.

Sources

- Indiana Code § 27-4-1-4.5[1], unfair claim settlement practices, Indiana General Assembly, accessed June 21, 2026.

- Indiana Code § 34-11-2-4[2], personal injury limitation period, Indiana General Assembly, accessed June 21, 2026.

- Indiana Code chapter 34-51-2, Comparative Fault Act, Indiana General Assembly, accessed June 21, 2026.

- Indiana Department of Insurance, consumer complaint resources, accessed June 21, 2026.